Bookkeeping

Accounting and the Importance of Adjusting Entries Chron com

Contents:

At the end of an accounting period during which an asset is depreciated, the total accumulated depreciation amount changes on your balance sheet. And each time you pay depreciation, it shows up as an expense on your income statement. Note that not all entries that the company records at the end of an accounting period are adjusting entries. For instance, an entry for sale on the last day of the accounting period does not make it an adjusting.

The GoCardless content team comprises a group of subject-matter experts in multiple fields from across GoCardless. The authors and reviewers work in the sales, marketing, legal, and finance departments. All have in-depth knowledge and experience in various aspects of payment scheme technology and the operating rules applicable to each. The team holds expertise in the well-established payment schemes such as UK Direct Debit, the European SEPA scheme, and the US ACH scheme, as well as in schemes operating in Scandinavia, Australia, and New Zealand. In accounting, the two bookkeeping methods are the single-entry and double-entry bookkeeping systems.

Best controller for F1 23 – Top picks for PlayStation, Xbox, and PC – RacingGamesGG

Best controller for F1 23 – Top picks for PlayStation, Xbox, and PC.

Posted: Fri, 10 Mar 2023 10:10:19 GMT [source]

This is posted to the Interest Receivable T-account on the debit side . This is posted to the Interest Revenue T-account on the credit side . In the journal entry, Depreciation Expense–Equipment has a debit of $75. This is posted to the Depreciation Expense–Equipment T-account on the debit side . Accumulated Depreciation–Equipment has a credit balance of $75.

Interested in automating the way you get paid? GoCardless can help

Our partners cannot pay us to guarantee favorable reviews of their products or services. We believe everyone should be able to make financial decisions with confidence. Thus these entries are very important for the representation of the accurate financial health of the company. However, one simple approach is called the straight-line method, where an equal amount of asset cost is assigned to each year of service life. You might wonder how the allowance account can develop a debit balance before adjustment.

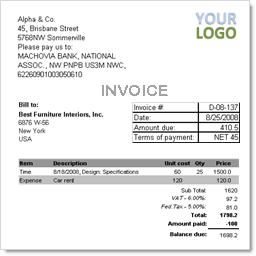

Adjusting entries are designed to make sure that the financial statements of a company accurately reflect its financial position. They usually involve shifting or reclassifying amounts from one account to another and are necessary for a variety of reasons. In this article, we will be discussing why adjusting entries are important. Depreciation is always a fixed cost, and does not negatively affect your cash flow statement, but your balance sheet would show accumulated depreciation as a contra account under fixed assets. If adjusting entries are not made, those statements, such as your balance sheet, profit and loss statement, and cash flow statement will not be accurate. Adjusting entries are made at the end of an accounting period to properly account for income and expenses not yet recorded in your general ledger, and should be completed prior to closing the accounting period.

Purpose of Adjusting Entries

It saves you https://bookkeeping-reviews.com/, money and keep the related debit with its credit in a single journal. It is if you decide to pay something in advance like your office rent for the rest of the year. Since your rent is $12,000, you will have to record the $1,000 for the rent expenses. There are different types of adjusting entries that are accruals, deferrals, and estimates. That money is recorded as accounts receivable in September, as you’re expected to get paid but have yet to receive the income. Then, in October, you record the money as cash deposited in your bank account.

- https://maximarkets.world/wp-content/uploads/2021/06/platform-maximarkets-5.jpg

- https://maximarkets.world/wp-content/uploads/2021/06/platform-maximarkets-4.jpg

- https://maximarkets.world/wp-content/uploads/2020/08/forex_trader.jpg

- https://maximarkets.world/wp-content/uploads/2019/03/Platform-maximarkets-2.jpg

- https://maximarkets.world/wp-content/uploads/2021/06/platform-maximarkets-all.jpg

However, his employees will work two additional days in March that were not included in the March 27 payroll. Tim will have to accrue that expense, since his employees will not be paid for those two days until April. Payroll expenses are usually entered as a reversing entry, so that the accrual can be reversed when the actual expenses are paid. An accrued expense is an expense that has been incurred before it has been paid. For example, Tim owns a small supermarket, and pays his employers bi-weekly.

Understanding Adjusting Journal Entries

The inventory balance on the balance sheet would be adjusted to reflect the amount of inventory that was counted in the company’s warehouse. Since inventory increased, we would debit inventory and credit cost of goods sold . A company maintains an allowance for bad debt reserve for any gross accounts receivable amounts that the company will not collect. A company will often calculate the required allowance for bad debt reserve at the of the period and an adjustment will be made to the current balance.

Financial StatementsFinancial statements are written reports prepared by a company’s management to present the company’s financial affairs over a given period . In other words, Prepaid expenses are expenditures that have not yet been recorded as expenses but already have been paid for. They are initially recorded as Assets when they are bought, and in the later accounting time period they are spent , their yielding potential realized. In other words, accrued revenue is a revenue that has been earned by selling goods and/or services, but for which no cash has been received. It is marked as Receivable on the Balance Sheet to represent cash that is being owed to the business.

- https://maximarkets.world/wp-content/uploads/2020/08/forex_education.jpg

- https://maximarkets.world/wp-content/uploads/2019/03/MetaTrader4_maximarkets.jpg

- https://maximarkets.world/wp-content/uploads/2020/08/logo-1.png

Automate, optimize, and manage intercompany non-trade transactions. Label each of the following as a deferral or an accrual, and explain your answer. Since Printing Plus has yet to collect this interest revenue, it is considered a receivable. This depreciation will impact the Accumulated Depreciation–Equipment account and the Depreciation Expense–Equipment account. While we are not doing depreciation calculations here, you will come across more complex calculations in the future. Recall the transactions for Printing Plus discussed in Analyzing and Recording Transactions.

In practice, you are more likely to encounter deferrals than accruals in your small business. The most common deferrals are prepaid expenses and unearned revenues. These three situations illustrate why adjusting entries need to be entered in the accounting software in order to have accurate financial statements. Unfortunately the accounting software cannot compute the amounts needed for the adjusting entries.

Explore the future of accounting marketing over a cup of coffee with our curated collection of white papers and ebooks written to help you consider how you will transform your people, process, and technology. From onboarding to financial operations excellence, our customer success management team helps you unlock measurable value. Through workshops, webinars, digital success options, tips and tricks, and more, you will develop leading-practice processes and strategies to propel your organization forward.

The revenue cycle refers to the entirety of a company’s ordering process from the time an order is placed until an invoice is paid and settled. The inability to apply payments on time and accurately can not only lock up cash, but also negatively impact future sales and the overall customer experience. Adjusting entries are necessary to ensure that the financial statements presented are accurate and in accordance with Generally Accepted Accounting Principles . It is also used to convert cash basis accounting to accrual basis accounting.

As the business provides the service/goods, the liability account is reduced and the corresponding revenue account is increased . It is normal to make entries in the accounting records on a cash basis (i.e., revenues and expenses actually received and paid). As an example, assume a construction company begins construction in one period but does not invoice the customer until the work is complete in six months. The construction company will need to do an adjusting journal entry at the end of each of the months to recognize revenue for 1/6 of the amount that will be invoiced at the six-month point. Second, adjusting entries are necessary for preparing financial statements in accordance with generally accepted accounting principles . GAAP requires that companies follow certain rules and guidelines when recording and reporting their financial information, and adjusting entries are an important part of this process.

You will notice there is already a debit balance in this account from the January 20 employee salary expense. The $1,500 debit is added to the $3,600 debit to get a final balance of $5,100 . This is posted to the Salaries Payable T-account on the credit side . This is posted to the Supplies Expense T-account on the debit side . You will notice there is already a debit balance in this account from the purchase of supplies on January 30. The $100 is deducted from $500 to get a final debit balance of $400.

These entries are so important because after this net profit or loss and financial position can be recognized in same accounting period . Adjusting entries are an essential part of accurate accounting under the accrual method. Once all the adjusting entries are added to a particular accounting period, you can complete the financial statements for that period and use them to plan for the financial future of your business. The primary distinction between cash and accrual accounting is in the timing of when expenses and revenues are recognized. With cash accounting, this occurs only when money is received for goods or services.

Accrued revenues may accumulate over time, some examples include interest, and services completed but a bill has yet to be sent to the customer at the end of the accounting period. Adjusting entries for accrued expenses can help you in more than one way. First, it will prevent you from spending money that has already been allocated for something else. Continuing with the example from above, you allocated the money to pay the vendor in the month of March. If the money does not leave the account in March, and you fail to record the accrued expense, it will look like that money is available for something else when you start the next accounting period. Second, adjusting entries for accrued expenses can help you more accurately forecast for future needs.

Xero Shoes Size Guide How to Fit Your Xero’s

On their website, they are said to be true to size, so I ordered a pair of EU 46 . If you are a woman and think of your foot as particularly wide, you can consider ordering a men’s style. Many female customers find a great fit in our men’s styles.

The 8 Best Shoes at Outdoor Retailer Winter Market 2020 – Footwear News

The 8 Best Shoes at Outdoor Retailer Winter Market 2020.

Posted: Thu, 30 Jan 2020 08:00:00 GMT [source]

The soles of the Genesis, original Cloud and Z-Trek are very thin and flexible. That’s why we offer free exchanges for all US orders. By following the instructions below, you’ll get the correct fit for your Amuri Venture or Cloud sandals. Steven contacted me shortly after my post and provided excellent customer service. I have been a dedicated consumer and strong supporter of Xero Shoes ever since. I even recommended them in a subsequent edition of my book.

Men’s Xero Shoe Size Tips

If you are still unsure of which size to order, we recommend ordering two sizes to try and keep the size you prefer. Xero Shoes tend to run wider than conventional shoes. If you normally wear a larger length shoe to get a wider fit, you’ll likely not have to do so when purchasing Xero Shoes. Note that natural materials may stretch during initial wear.

- You’ll use this measurement to select the right size of our DIY kits.

- This step is very important for getting a great fit the first time.

- This will give you a good idea of your size… but PLEASE follow the next step whenever possible.

If you think of your foot is a bit longer than the kids size 4, you can consider ordering the narrower but longer women’s style. We’re happy to offer free domestic returns and exchanges for unworn shoes and sandals within 45 days of purchase. Xero shoes have a model called Alpine, for snowy conditions.

Men’s Shoes

I love how I can see your tan line from the shoes! You’re definitely a supporter of your own product. You’ll use this measurement to select the right size of our DIY kits.

- Many male customers find a great fit in the women’s styles.

- Like I think my foot size would be more of a 13.5 but the 14’s fit me perfectly.

- All of our children’s shoes are wider than conventional children’s shoes.

- If you think of your foot as particularly wide, you can consider ordering a men’s style.

- Many female customers find a great fit in our men’s styles.

This will give you a good idea of your size… but PLEASE follow the next step whenever possible. Take a ruler and measure from the edge of the paper to the mark you made. Place a piece of paper against a wall (if you have VERY large feet, use a piece of newspaper. I’ve now checked through shoes from more than 10 brands, and 11,5 is shown as 46. Literally every other shoe I own, every pair from multiple brands , show that EU 46 is 11,5. Early this spring I decided to switch to zero drop shoes (+phasing to more barefoot running etc).

Xero Shoes Size Guide

I liked them so much I bought a pair of the all weather-version as well. Here’s a quick video showing you how to https://bookkeeping-reviews.com/ your feet and get the correct size for your Xero Shoes DIY sandal kits. Below are general tips and considerations for selecting your Xero Shoe size. We hope this guide will further assist you in your Xero shoe buying experience.

Arc’teryx Beta FL Hardshell Jacket Review – The Trek

Arc’teryx Beta FL Hardshell Jacket Review.

Posted: Tue, 30 Mar 2021 07:00:00 GMT [source]

Verify the fit by printing the appropriate size template and comparing it to your foot. This step is very important for getting a great fit the first time. The hemp canvas casual cool-weather boot with faux-shearling for women.

All of Xero women’s shoes are wider than conventional women’s shoes. If you normally wear a larger size to get a wider fit in conventional shoes, you may not have to do that with Xero Shoes. Be aware that natural materials may stretch during initial wear. If you think of your foot as particularly wide, you can consider ordering a men’s style. Many female customers find a great fit in men’s styles. Just be sure to adjust the size by 1.5 (for example a men’s 7 is the same as a women’s 8.5).

All of our children’s shoes are wider than conventional children’s shoes. All Xero’s shoes are wider than conventional shoes. Many of our female customers find a great fit in our men’s styles. Just be sure to adjust the size by 1 (for example a women’s 39 is the same length as the wider men’s 40 in our shoes). Many of our male customers find a great fit in our women’s styles. Just be sure to adjust the size by 1 (for example a men’s 40 is the same length as the narrower women’s 39 in our shoes).

Shoe sizing, especially online, is not a perfect process. That’s why we offer free exchanges for all orders. You can read our full return/exchange policy here. Since snowy times are fast approaching, I’ve been on the lookout for a pair of good “natural shoes” for the cold. The size was “true to size” in my experience and I got a pair in Eu size 46, which gave my toes some space.

Size Charts and Templates

An eco-friendly road running shoe made with sustainable materials.

Just be sure to adjust the size by 1.5 (for example a men’s 7 is roughly the same as a women’s 8.5). If you are a man and think of your foot as particularly narrow, you can consider ordering a women’s style. Many male customers find a great fit in women’s styles. For example, a men’s 41 is the same exact shoe as a women’s 39.5. In my opinion I find Xero to run a little bit small compared to other barefoot shoes.

If you think of your foot as particularly narrow, you can consider ordering a accountant & bookkeeper guides style. Many male customers find a great fit in the women’s styles. All of our women’s shoes are wider than conventional women’s shoes. All of our men’s shoes are wider than conventional men’s shoes. All of Xero Shoe’s children’s shoes are wider than conventional children’s shoes.

Like I think my foot size would be more of a 13.5 but the 14’s fit me perfectly. The sole of the Z-Trail is thicker than our other sandals, so customers can get a roomier fit on this style, if preferred. The Genesis and the original Cloud are unisex styles. For example a men’s 7 is the same exact shoe as a women’s 8.

شموع

شموع